Skip to main content Skip to footer

Skip to main content Skip to footer VAT Registration in Bahrain - Registered, Filed, and Kept Compliant

For foreign-owned companies in Bahrain that need VAT handled correctly from the initial NBR registration through every quarterly return.

In This Guide

Does Your Company Need to Register for VAT?

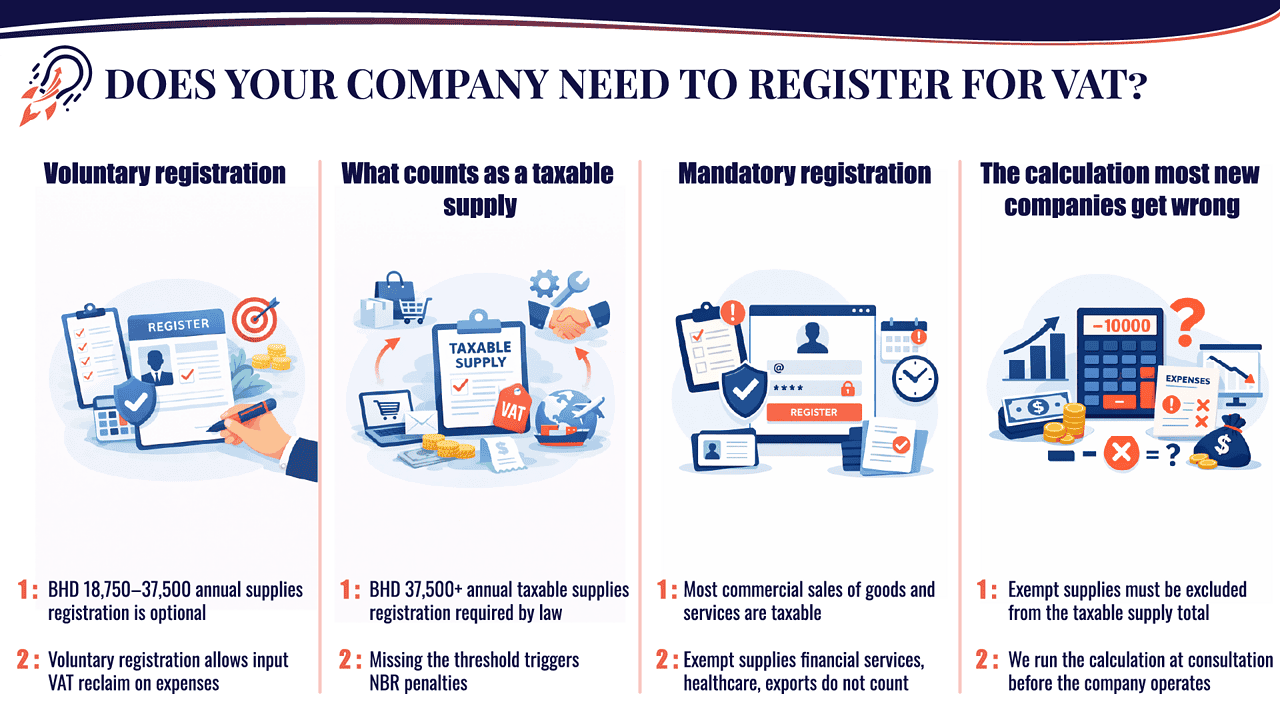

Voluntary registration

BHD 18,750 If your annual taxable supplies are between BHD 18,750 and BHD 37,500, you can choose to register voluntarily. Many companies do particularly those with significant input VAT on their expenses. Registered companies can reclaim input VAT paid on business purchases, which for capital-intensive businesses can be a meaningful sum.

Below BHD 18,750 No registration option. The company cannot charge VAT and cannot reclaim input VAT.

What counts as a taxable supply

This is where the complexity starts. Taxable supplies include most standard commercial sales of goods and services. They do not include exempt supplies (certain financial services, residential property, local passenger transport) or zero-rated supplies (exports outside the GCC, certain healthcare and educational services). Getting this calculation right matters both for determining whether you have crossed a threshold and for calculating how much VAT you actually owe on each return.

Mandatory registration

BHD 37,500 If your company’s annual taxable supplies exceed BHD 37,500, you are legally required to register for VAT with the National Bureau for Revenue. This applies to supplies made in Bahrain or to Bahrain-based customers. Missing the mandatory registration threshold triggers penalties from NBR, and NBR’s enforcement on this has become more active since 2022.

The calculation most new companies get wrong

Including exempt supplies in their taxable supply total when determining registration eligibility. Exempt supplies do not count toward the threshold. A company with BHD 50,000 in total revenue, of which BHD 20,000 is exempt, has BHD 30,000 in taxable supplies below the mandatory threshold. We run this calculation at the initial consultation so the company knows its position before operating for a full year.

What VAT Registration Involves - The NBR Process

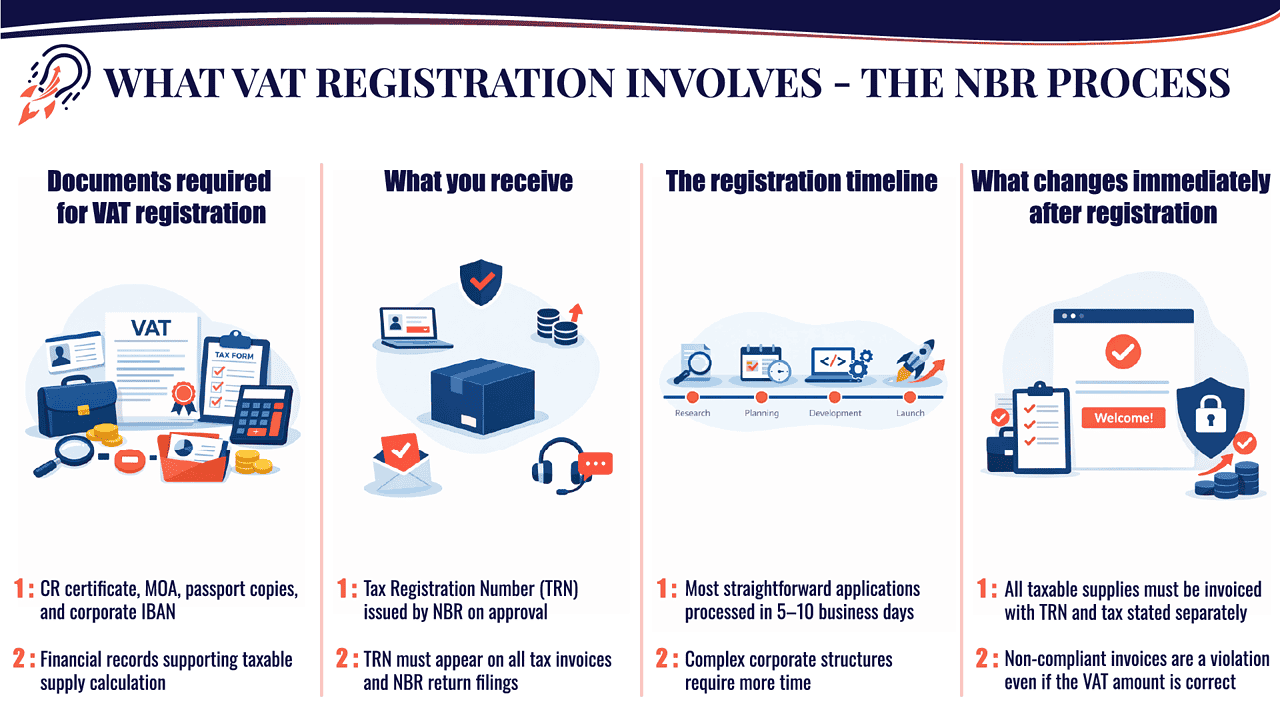

Documents required for VAT registration

- Commercial Registration (CR) certificate – current

- Memorandum of Association (MOA)

- Valid passport copies of all authorised signatories

- Company bank account details – IBAN from your Bahrain corporate account

- Financial records supporting your taxable supply calculation – invoices, contracts, or projected revenue documentation

- Authorisation letter appointing PI Startup Advisory as your tax representative (where applicable)

What you receive

Once approved, NBR issues a Tax Registration Number (TRN). This number must appear on all tax invoices your company issues. It also appears on your NBR account where all return filings are submitted.

The registration timeline

NBR processes most straightforward VAT registration applications within 5-10 business days. Applications that require additional verification – particularly for companies with complex corporate shareholder structures or financial services activities – can take longer. We follow up directly with NBR through the tax representative channel to resolve any queries without delays cascading from an unanswered email.

What changes immediately after registration

You are required to issue tax invoices (not just standard invoices) for all taxable supplies. Tax invoices have specific format requirements under Bahrain’s VAT Executive Regulations – TRN number, tax amount stated separately, date, sequential invoice number. Issuing non-compliant invoices is a violation, even if the VAT amount itself is correct.

VAT Rates - What Is Taxed, What Is Not

Standard-rated - 10%

Most commercial goods and services supplied in Bahrain. Consulting fees, professional services, retail sales, office supplies, software subscriptions, hospitality, and most business-to-business transactions.

Zero-rated - 0% (VAT charged but at 0%)

Zero-rated supplies are still taxable — they just carry a 0% rate. This means they count toward your taxable supply threshold and can be included in input VAT claims. Examples relevant to foreign-owned companies in Bahrain:

- Exports of goods outside the GCC

- International transport services

- Certain healthcare goods and medicines

- Supply of crude oil and natural gas (sector-specific)

Zero-rated is not the same as exempt. This distinction catches companies out regularly.

Exempt - No VAT

Exempt supplies are outside the VAT system entirely. You do not charge VAT on them and you cannot reclaim input VAT related to them. Examples:

- Certain financial services (specific to regulated financial activities)

- Local residential property transactions

- Bare land sales

- Local passenger transport

Why this matters for your quarterly return

Quarterly VAT Filing - What It Involves

What a quarterly return calculates:

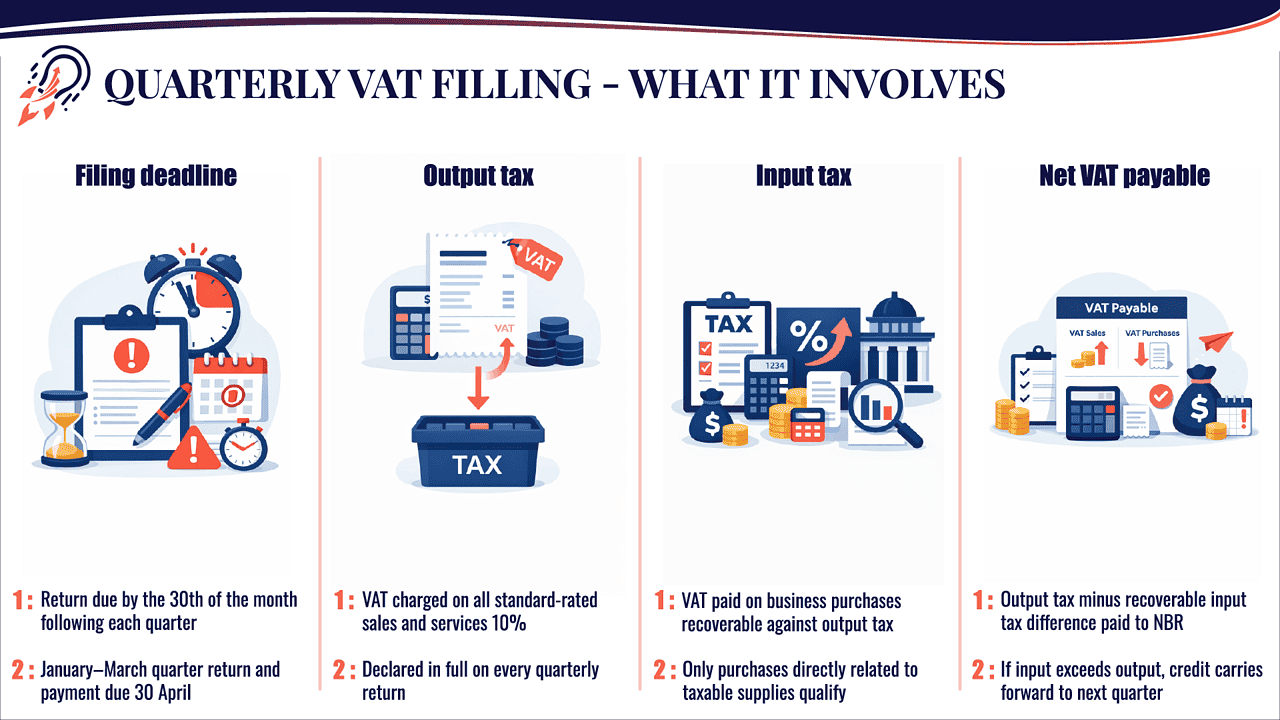

Filing deadline

The 30th day of the month following the end of the tax period. For a January-March quarter, the return and payment are due by 30 April.

Output tax

The VAT you charged on your sales and services during the quarter. 10% of every standard-rated supply issued.

Input tax

The VAT you paid on your business purchases during the quarter. Recoverable against your output tax liability.

Net VAT payable

Output tax minus recoverable input tax. If your output tax exceeds your input tax, you pay the difference to NBR. If your input tax exceeds output tax (common in early trading periods when capital expenses are high), you carry the credit forward or apply for a refund.

Late filing penalty

BHD 500 for a first late filing. Increasing penalties for repeat late filings. NBR also charges interest on late payments at the rate set in the VAT Executive Regulations.

What we do on every quarterly filing:

The most common error in quarterly filings is not the calculation — it is missing invoices. An invoice that did not make it into the records means underreported output tax, which NBR can identify through cross-referencing with your counterparties' returns. We establish a monthly document collection routine with clients to ensure nothing is outstanding by the time the filing window opens.

Common VAT Compliance Mistakes and How We Prevent Them

Including exempt supplies in the registration threshold calculation

As noted earlier, exempt supplies do not count toward the BHD 37,500 mandatory registration threshold. A company that incorrectly includes exempt revenue in its threshold calculation may believe it is required to register when it is not – or in the other direction, may not register when it should. Both create problems. We run the correct calculation before advising on registration.

Issuing standard invoices instead of tax invoices

A standard invoice is not a tax invoice under Bahrain’s VAT law. After registration, every taxable supply requires a tax invoice with specific mandatory fields. Missing the TRN, failing to state the VAT amount separately, or using non-sequential invoice numbers are all violations, even if the VAT amount itself is correct. We provide a compliant tax invoice template at registration.

Inadequate record keeping

NBR requires VAT records to be kept for 5 years from the end of the tax period they relate to. This includes all tax invoices issued and received, customs records for imported goods, and documentation supporting any adjustments made in returns. Missing records during an NBR audit creates significant exposure.

Claiming full input VAT on mixed-supply businesses

If your company makes both taxable and exempt supplies, your input VAT recovery is restricted proportionally. Claiming 100% when your taxable activity is 60% of total revenue means you have overclaimed, and NBR will identify this. We calculate the partial exemption ratio on every return.

Missing the registration window

Companies that cross the BHD 37,500 threshold without registering promptly face backdated VAT liability and penalties from NBR. We monitor taxable supply levels for clients and flag the approaching threshold before it is crossed.

Late or missing quarterly filings

The NBR deadline is firm. BHD 500 for the first late filing. Repeat violations increase the penalty. We file every return before the deadline, not on the deadline. Clients receive a draft return for review 7 business days before submission is due.

VAT and Your Company Registration Package

What a quarterly return calculates:

What is included in the VAT registration service (standalone or as part of Platinum):

- Taxable supply threshold assessment — confirming whether registration is mandatory or voluntary for your specific business model

- NBR portal registration — end-to-end application and TRN issuance

- Tax invoice template preparation — compliant format for immediate use after registration

- Quarterly VAT return filing — for the first year, with handover or continuation option at renewal

- NBR query management — we respond to any NBR enquiries during the registration and first filing period

- Record keeping guidance — document retention schedule and filing system setup

Standalone VAT service — ongoing quarterly filing:

Frequently Asked Questions

Is VAT registration mandatory for my company?

It depends on your annual taxable supplies, not your total revenue. If taxable supplies exceed BHD 37,500 per year, registration is mandatory. Between BHD 18,750 and BHD 37,500, it is voluntary. Below BHD 18,750, registration is not available. The calculation of taxable supplies excludes exempt activities, which is where most companies make the mistake. We run this assessment at the initial consultation based on your actual or projected business activity.

How long does NBR take to process a VAT registration?

Standard applications are processed within 5-10 business days. Applications involving complex corporate structures, regulated activities, or incomplete documentation take longer. We submit complete applications with all supporting documentation on the first attempt to avoid the back-and-forth that extends this timeline.

What is the difference between zero-rated and exempt supplies?

Zero-rated supplies carry 0% VAT they are still taxable supplies, count toward your registration threshold, and allow you to reclaim related input VAT. Exempt supplies are outside the VAT system entirely; they do not count toward your threshold and do not allow input VAT recovery on related costs. This distinction affects your quarterly return calculation, your registration eligibility, and your input tax claims.

When do I need to start charging VAT after registration?

From the effective date of your VAT registration as confirmed by NBR. Not from the date you applied, but from the date NBR confirms the registration. Charging VAT before your TRN is confirmed, or failing to charge it after confirmation, are both compliance errors.

Can I reclaim VAT on expenses before my company was registered?

In some circumstances, yes. Bahrain’s VAT law allows recovery of input VAT paid on goods and services acquired before registration, provided those goods and services are used in making taxable supplies after registration. The rules on pre-registration input VAT recovery are specific; we assess eligibility on a case-by-case basis and include any valid pre-registration claims in the first quarterly return.

What happens if my company does not file a VAT return on time?

NBR charges a BHD 500 penalty for the first late filing. Penalties increase for subsequent late filings. Interest accrues on any VAT paid after the due date. In serious cases of non-compliance, NBR can deregister a company or refer the matter for further enforcement action. We file every return before the deadline, not on it. Clients receive a draft return for review 7 business days before submission.